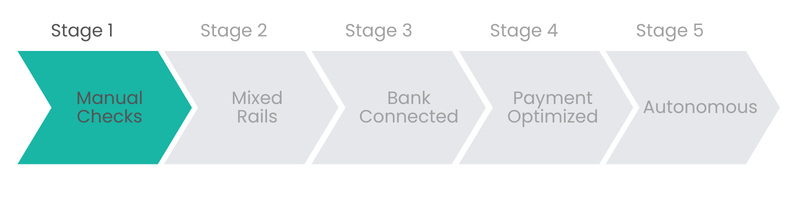

From Manual Checks to Autonomous Payment Optimization

Finance teams have modernized their ERPs.

They’ve integrated with banks.

They’ve adopted ACH and digital payment rails.

And yet, payments still feel manual. Why?

Because most organizations optimize processing, not payment decisioning.

This is where the payments maturity journey becomes critical. It maps how organizations evolve from manual check printing to fully autonomous, policy-driven payment optimization and, why many teams stall in the middle.

If you're evaluating AP automation, digital payment transformation, or ways to reduce payment costs and fraud risk, understanding where you sit on this curve is the first step.

Stage 1: Manual Checks (Paper-Driven Payments)

What it looks like:

- Printing and signing checks manually

- Physical check stock management

- Mailing and remittance handling

- Manual reconciliation

Risks and limitations:

- High cost per check

- Fraud exposure

- Slow settlement timing

- Limited payment tracking visibility

Manual check workflows don’t scale. As volume grows, so do operational costs and exception handling.

Stage 2: Fragmented Payments (Mixed Digital + Checks)

.png)

What it looks like:

The problem:

Digital rails reduce costs, but fragmentation increases complexity.

You now manage:

- Vendor payment preferences manually

- Routing and account collection processes

- Separate tracking systems

More rails ≠ more optimization.

Stage 3: Bank-Connected Payments (Batched + Integrated)

.png)

What it looks like:

- ERP-to-bank integrations

- Batched payment processing

- Stronger approval controls

- Centralized disbursement files

This stage delivers:

- Greater efficiency

- Better audit controls

- Reduced manual entry

But payments are still static.

The payment rail is selected upfront.

Settlement timing is fixed.

Vendor preferences are not dynamically captured.

Optimization doesn’t occur at the “last mile.”

Bank-connected improves control, but not flexibility.

Stage 4: Payment-Optimized (Dynamic Rail Decisioning)

.png)

Instead of locking in a payment method at creation, organizations introduce a decisioning layer that optimizes:

- Payment rail (ACH, check, RTP, wire)

- Settlement timing (standard vs accelerated)

- Policy rules (amount thresholds, vendor type, risk profile)

What payment optimization enables:

- Rail switching (check → digital conversion)

- Cost reduction through rule-based routing

- Faster vendor settlement when needed

- Reduced exceptions

- Improved vendor experience

Payments move from static transactions to intelligent workflows.

Stage 5: Autonomous Payments (Policy-Managed + Risk-Aware)

.png)

What it includes:

- Risk scoring of payees

- Real-time rail availability awareness

- Dynamic timing decisions

- Early pay / discount management

- AI-driven policy enforcement

The outcome:

Best rail. Best timing. Lowest risk. Automatically.

Autonomous payments aren’t about eliminating humans, they’re about removing repetitive payment decisions from human workflows.

Where Most Organizations Are Today

.png)

They’ve:

- Reduced manual checks

- Connected to banks

- Standardized batching

But they haven’t introduced:

- Dynamic rail selection

- Settlement optimization

- Embedded payee preference capture

- Risk-aware routing

That’s the gap between digital payments and payment optimization.

Why This Matters for AP Automation and Treasury Teams

Modern AP automation shouldn’t just:

- Generate payments

- Send files to a bank

- Track status

It should:

- Optimize cost per payment

- Improve working capital flexibility

- Reduce fraud risk

- Enhance vendor experience

- Minimize reconciliation friction

Payment maturity directly impacts:

- Operational efficiency

- Fraud exposure

- Vendor satisfaction

- Cash flow strategy

How to Identify Your Current Payment Maturity Stage

Ask:

- Is the payment rail chosen before vendor interaction?

- Do you manually manage vendor payment preferences?

- Can you change settlement timing dynamically?

- Are policy rules embedded in workflows?

- Do you monitor risk at the payee level?

If most answers are “no,” you’re likely bank-connected, but not payment-optimized.

The Next Step: Moving from Processing to Decisioning

Digital transformation in payments isn’t about adding more rails.

It’s about adding intelligence between initiation and disbursement.

Organizations that introduce payment optimization gain:

- Lower payment costs

- Faster settlement options

- Reduced fraud exposure

- Better vendor flexibility

- Stronger operational control

And that’s where the real competitive advantage emerges.

Final Thought

The payments maturity journey isn’t about replacing systems overnight.

It’s about understanding your current stage, and taking the next strategic step toward smarter, more autonomous payment workflows.

If you're evaluating ways to improve AP automation, payment security, digital disbursements, or vendor payment optimization, mapping your maturity level is the most practical place to begin.

.jpg)

.jpg)